Legislation that draws a distinction between wholesale and retail clients is aimed squarely at bolstering protection for retail clients in the financial advice process. At the same time, allowing clients to be classified as wholesale enables those with the skills, desire and experience to participate in wholesale markets, and invest in more complex products.

For advisers, the distinction is important, not only because the compliance obligations and advice process differs significantly between these two types of clients, but also because the investment opportunities and access to certain products also differ.

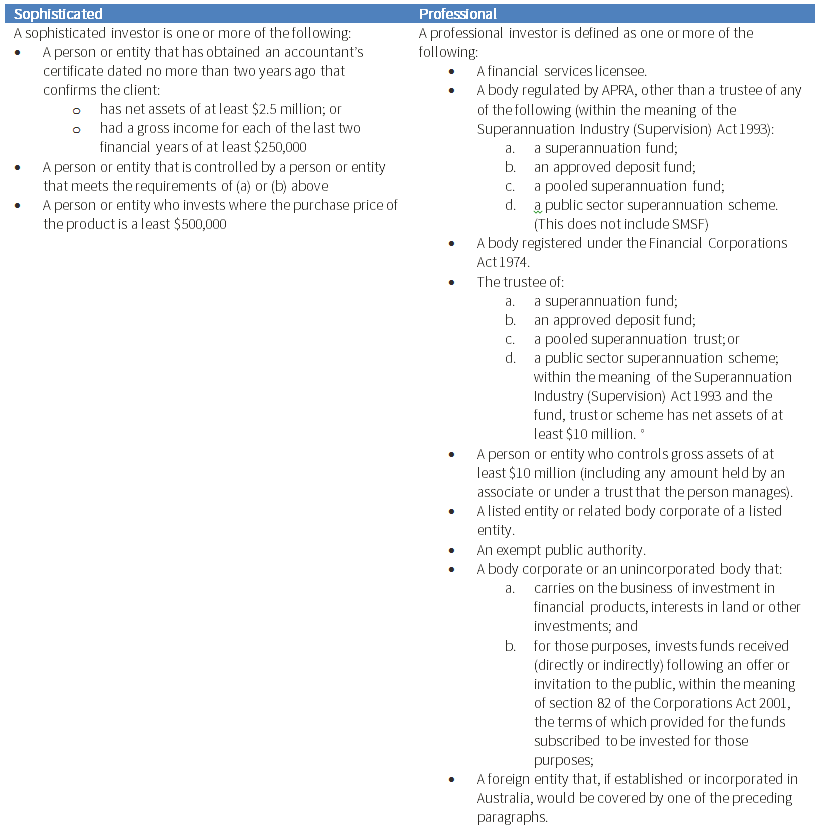

What is a wholesale client?

Essentially, everyone is a retail client unless they satisfy one of the requirements to be classified as a wholesale client under the Corporations Act 2001 Act (Corporations Act).

There are a few categories of wholesale clients under the Act. Here are a few of the most common ones:

- A person or entity that has obtained a qualified accountant’s certificate stating they have net assets of at least $2.5 million, or a gross income for each of the last two financial years of at least $250,000. The certificate lasts for two years before it needs to be renewed.

- A professional investor, which includes, among others, financial services licensees, bodies regulated by APRA, superannuation funds, as well as a person or entity who controls gross assets of at least $10 million (including any amount held by an associate or under a trust that the person manages).

What are the key differences?

The law is less prescriptive about the advice process for wholesale clients compared to retail clients, which means compliance obligations are greatly reduced.

- Retail clients must receive a Financial Services Guide (FSG), Statement of Advice (SOA) and where appropriate, a Product Disclosure Statement (PDS) from their adviser. Wholesale clients are not required to receive any of these documents.

- Retail clients enjoy all of the consumer protections set out in the Future of Financial Advice (FOFA) reforms. Wholesale clients generally do not.

- Wholesale clients have access to a wider range of investments and products compared to retail clients.

Why is the distinction important?

The tests for wholesale clients are clearly aimed at financially savvy, informed and confident investors with experience in protecting their interests. However, wealth is not always a good proxy for financial literacy. Added to that, when a client is classified and treated as ‘wholesale’, they lose access to important protections set out in the Corporations Act as well as access to external dispute resolution schemes, which they may not be aware of.

It’s important to recognise that while a particular client might meet a monetary threshold to be classified as ‘wholesale’, they may not have sufficient experience or investment knowledge to confidently make financial decisions. For example, owning a house, receiving an inheritance or building up a business in a certain industry does not necessarily equip clients with the right know-how when it comes to investing and making financial decisions to secure their future. In these scenarios, it’s up to you as their adviser to use your professional judgement to determine if it would be a better experience for the client to go through the retail advice process instead.

What about self-managed super funds?

The implications for self-managed super funds (SMSFs) are still somewhat of a grey area. The relevant law states that a trustee of an SMSF will be classified as a retail client under the Act unless the fund holds net assets of at least $10 million at the time the service is provided.

This means that even though a client might qualify as wholesale under the usual tests, if they hold less than $10 million in their SMSF they have to be treated as a retail client when it comes to their super. This can lead to an unusual client experience where you provide advice in a wholesale fashion for non-super assets, and when advising on the SMSF you would need to provide a SOA and go through the full retail process.

However, if investment advice only is provided to the SMSF Trustee (for example, advice about investment opportunities in equities or other financial products), this can be provided on a wholesale advice basis provided the SMSF trustees meet the wholesale client test.